If you have been thinking about creating a money lending app, you may have noticed how this business has thrived in recent years. And indeed, more and more people choose mobile banking over managing their finances in traditional institutions due to many conveniences. However, a good performance on stage never shows all the hard work behind the curtains, and developing a loan app is no exception.

To make the application top-notch, safe, and fast, future app owners must take care of many security issues, pay attention to legal regulations, integrate third-party tools, and the list goes on! I have seen many times how these complications block our clients from evolving their ideas. But as a Product Manager, I assure you that you're not doomed to develop the loan app on your own.

Uptech is a software development company. We have been creating apps since 2016 and can help you build robust software and give your app a quality design! Feel free to contact us. Now, let's discover how to build a money-lending app.

A Quick Look at the Money Lending App Market

Before rushing to strike you with some statistics, I have to mention one of the key players contributing to financial digitalization. And it’s mobile banking apps.

Mobile banking was on the rise before the pandemic, but the spread of the virus increased the demand for remote financial services. According to the Boston Consulting Group survey, more than 40% of people between 18 and 34 years old started using online or mobile banking for the very first time as the pandemic broke out. A national survey shows that 54% of bank customers prefer to manage their accounts through mobile banking apps, while 22% use online banking via a laptop or PC as their main option.

So have advanced loan services. The global digital lending platform market was valued at $10.55 billion in 2024 and is expected to grow significantly, reaching $44.49 billion by 2030, with a 27.7% CAGR between 2025 and 2030. What's even more fascinating about these numbers is that major lending companies started hitting it big just recently, dominating the North American and European markets. The demand remains high in the Asia Pacific due to many emerging fintech companies in that region.

What Is a Money Lending App and Why Create One?

A money lending app is a digital product that allows people to apply for, receive, and repay loans directly from their phone or computer. Instead of visiting a bank branch, filling out paperwork, and waiting days for a response, borrowers submit a request online. The platform checks eligibility, evaluates risk, and issues a decision within minutes or hours.

These apps have become common across fintech. Some focus on small paycheck advances. Others provide personal loans or financing for small businesses. In all cases, the goal is the same: to remove friction from the lending process and make access to credit faster and easier.

Before we look at how to create a money lending app, it helps to understand why the model works so well.

People get money faster

Speed is one of the main reasons users choose lending apps. With a traditional bank loan, the process may take several days. A digital platform can review an application much faster because many checks happen automatically.

A person fills in basic information, confirms identity, and submits the request. The platform evaluates the data and returns a decision. In many cases, the funds appear the same day or the next business day.

Borrowing becomes easier to manage

Most lending apps break the loan process into a short and understandable flow. A user creates an account, provides financial details, reviews the terms, and confirms the request. After that, the app shows repayment dates, loan balance, and payment history.

For the user, this means fewer confusing steps. Everything related to the loan stays in one place.

Lenders can reach more users

A digital lending platform does not depend on physical offices. A company can launch a product and serve customers in multiple regions without opening branches.

This is one reason fintech companies entered the lending space so actively. With a well-built product, a lender can reach people who rarely interact with traditional banks, e.g., freelancers, gig workers, or small online businesses.

Lending decisions can improve over time

Digital products generate useful data. Payment history, account activity, and repayment patterns help lenders understand borrower behavior more clearly.

Over time, this information allows companies to refine risk models and adjust loan conditions. Instead of relying only on a traditional credit score, the platform can use a wider set of signals when evaluating applications.

The market keeps expanding

The digital lending sector has been growing steadily. Recent estimates show that the global digital lending platform market reached $10.55 billion in 2024 and may grow to $44.49 billion by 2030, with a 27.7% compound annual growth rate between 2025 and 2030.

For fintech startups and financial institutions, this growth signals strong demand for digital credit products.

In the next section, we’ll look at the practical side and walk through the main steps required to create a money lending app.

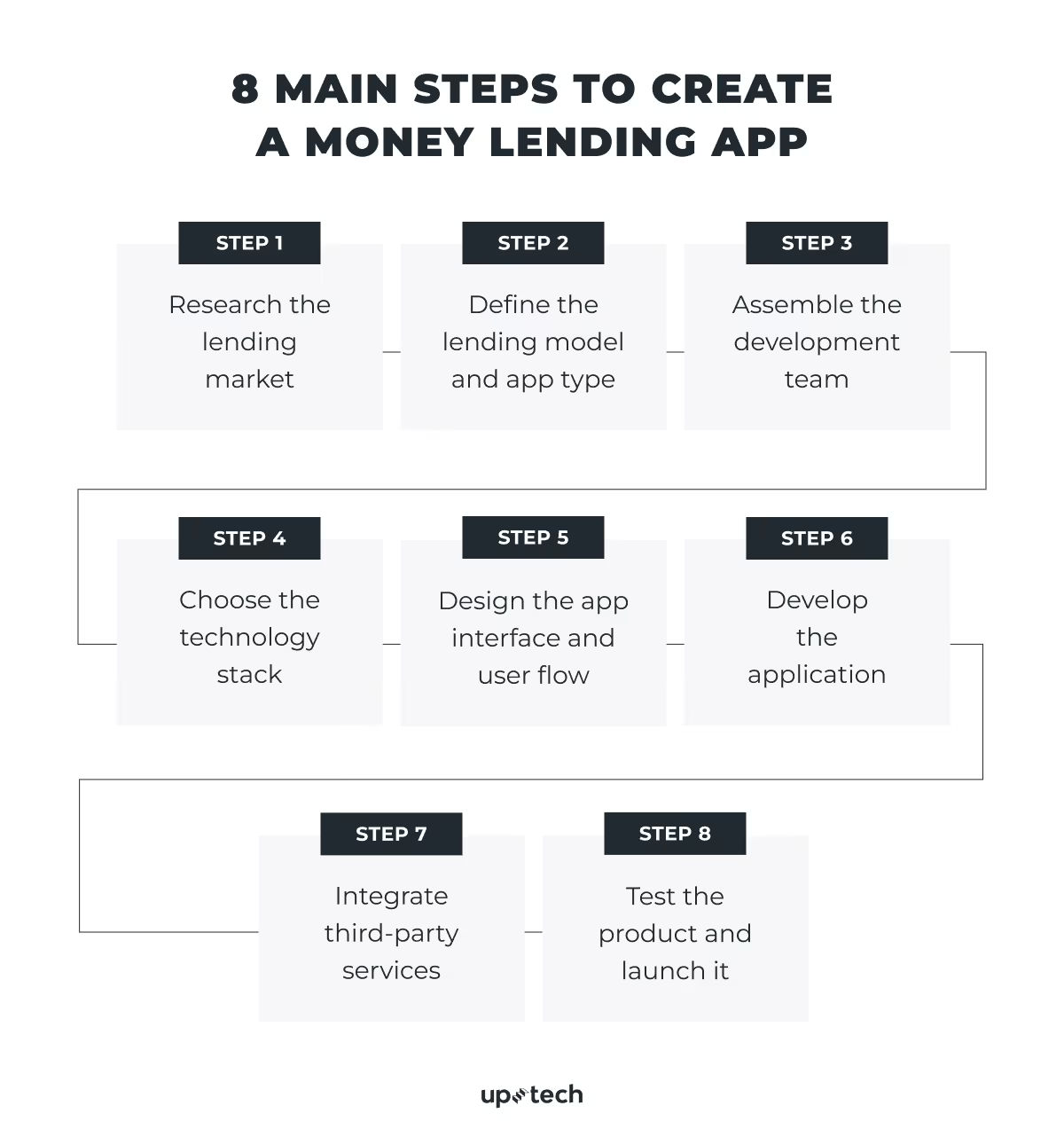

How to Create a Money Lending App: 8 Steps

A money lending app does not start with code. First comes the idea, the lending model, and the product decisions behind it. You need to understand the market, define the loan product, select the right technologies, and prepare the platform for security and compliance requirements.

At Uptech, we follow a structured product development approach to build fintech solutions. Over the years, this process has proved practical for teams that want to launch a lending product without unnecessary delays or costly mistakes.

Here are the key steps we usually take to create a money lending app:

- Research the lending market

- Define the lending model and app type

- Assemble the development team

- Choose the technology stack

- Design the app interface and user flow

- Develop the application

- Integrate third-party services

- Test the product and launch it

Below, we break down each step and explain what happens at every stage of the development process.

Step 1: Research the lending market

Take a good look at other lending apps, noting their strong and weak sides. Try out a few of them to gain first-hand experience. Otherwise, watch some lending app reviews on YouTube, and don't forget to read the comment section! You can find some valuable feedback from users about their experiences. This is the homework that will give you a bigger picture of the market you're going to enter.

Pay attention to the lending model behind each product in addition to user experience. Some apps provide paycheck advances, others offer personal installment loans, or act as marketplaces that connect borrowers with lenders. The model you choose will affect the product features, compliance requirements, and overall development scope.

It also helps to review the approval process, repayment structure, and fees used by competitors. This will give you a better sense of what users expect from a lending app and where there may still be room for improvement.

Step 2: Define the lending model and app type

After conducting market research, think of the crucial attributes you'd like your loan app to include.

There are a few different types of loan applications based on the size of the credit they can give. In practice, these categories also reflect how lending products work, how risk is assessed, and what repayment model the app supports.

As soon as you select a certain type, it will be much easier to estimate the cost and features of developing a money-lending app.

Small loans for cash advances

Usually, under $500, they work best for fast funding and charge minimal fees, offering automatic overdraft protection.

Chime or MoneyLion are money lending apps of this sort.

These apps usually provide short-term advances that help users cover expenses until the next paycheck. Approval often relies on income verification, payroll integrations, or bank transaction history instead of a traditional credit score.

Many solutions connect directly to the user’s bank account and automatically deduct repayment on the next payday. Some platforms also include budgeting tools, savings features, or subscription-based access instead of interest charges.

Small personal loans

Usually under $5,000. This type of money loan app is appropriate for those who need quick funding and have relatively low credit scores. Universal credit, for instance, grants access to personal loans ranging from $1,000 to $50,000, even if your credit is damaged. Among the leading platforms, I'll also mark LendingPoint, which doesn't take much time to let you register an account and issue the loan on the next day after confirmation.

Compared with cash advance apps, these platforms usually provide longer repayment periods that may range from several months to a few years. Approval often combines credit score checks with additional data such as income verification and banking activity. Many lending apps in this category include features such as loan calculators, repayment schedules, credit score monitoring, and automated payment reminders

Startup business loans

Usually, over $5,000. As you can guess from the name, these loans suit startup owners who aim to set their businesses in motion. Applications of this type, like Lendio or Bluevine, to name a few, give access to lines of credit, connecting your business to various lenders. Meanwhile, a good deal of loan applications are known to only operate in certain countries or states. Lendio is available worldwide, which is a win for both parties.

Many business lending platforms are marketplaces of some sort that connect companies with multiple lenders rather than issuing loans directly. This allows startups to compare offers, access working capital financing, or open business credit lines through one interface.

These platforms often include features such as loan comparison tools, financial document uploads, and integrations with accounting software.

Many factors, like app development cost, team, outsourced services, and future app features, will depend on the app type. At this stage, you should make your current plans and shape your ideas in a more realistic and practical framework.

Step 3: Assemble the development team

As you have an approximate plan on how to start a lending business, choose your squad to discuss the work strategies more thoroughly. Basically, you have four options here:

- Work with freelancers

- Take in-house

- Hire an outsourcing company

Each team type differs in price, starting from freelancers as the most affordable option and extending to a development agency as the most costly.

Freelancers may work well for small tasks or early experiments, but managing several independent specialists often requires more coordination from your side. An in-house team gives you full control over the product, although hiring and onboarding may take time.

When you outsource software development, you get a ready-made team that includes developers, designers, QA engineers, and product managers. This model helps launch development faster while keeping costs lower than maintaining a full internal team.

Many fintech startups choose outsourcing because it combines speed, product expertise, and predictable development costs.

Opting for an outsourcing team is an optimal solution regarding the costs, development speed, and quality. Check the comprehensive guide on how to find app developers for your project and how it benefits your business.

Step 4: Choose the technology stack

Now we've moved on to the practical step. Think of your web infrastructure and what technologies must be built within it to make it scalable and secure. These are the general points your team has to work on:

- app infrastructure;

- backend and frontend development;

- database management;

- UI/UX design.

A money lending app also needs a reliable architecture that can process loan applications, user verification, and payment transactions without delays. The technology stack should support stable performance as the number of users grows.

Though a money lending app isn’t a bank, it works with private user data, so security should be taken seriously. The users’ data should be encrypted at rest and in transit. You should use the best security practices to protect the system from hackers. Data backup, penetration testing, metadata tracking, etc., are the fintech security practices we at Uptech use.

It is also common to integrate identity verification tools, fraud detection systems, and payment providers directly into the platform. These integrations help automate risk checks and keep transactions secure.

Overall, it all comes down to having a trusted and professional development team. We at Uptech have been working on fintech products like GreenFi and Cardless, so we know how to build a secure fintech solution, indicate security weaknesses, and fix them.

Step 5: Design the app experience

While a good design won't make a killing, a bad design can be a real buzzkill for the target audience. Try to keep the interface simple so that the app is easy to navigate. Borrowers should understand how to apply for a loan, review terms, and check repayment details without confusion.

Most lending apps focus on a short and clear user flow: account creation, identity verification, loan application, and repayment management. The fewer steps the user needs to complete, the higher the chances they will finish the application.

Also, consider adding gamification; it might come in handy when your users receive credit points. Some fintech apps use reward systems, progress indicators, or credit score improvements to keep users engaged and encourage responsible repayment behavior.

Step 6: Develop the application

Development of a money lending app usually includes several parallel tracks, from product logic to user-facing functionality and system integrations.

Front-end development

This part focuses on creating the user interface, which involves designing and developing the app's layout, menus, buttons, and other elements that the user interacts with. The front-end development team also creates the app's web pages, which are built using technologies such as HTML, CSS, and JavaScript.

At this stage, the team also works on key lending flows such as registration, identity verification, loan application forms, approval status, repayment tracking, and notifications.

Back-end development

This part is concerned with the server-side of the app, where the data and logic of the app are stored. This includes developing the database schema and building APIs that allow the front-end of the app to communicate with the back-end. Back-end development teams typically use programming languages such as Python, Ruby, or Java, and database management systems like MySQL.

For a lending product, the backend also handles user authentication, credit checks, loan calculations, repayment schedules, transaction records, and integrations with third-party services.

Overall, the development process of a money lending app involves a combination of front-end and back-end development, which together create a user-friendly, secure, and efficient platform for managing loans and financial transactions.

If the product includes both a borrower app and an admin panel, the team usually builds both parts in parallel so lenders can review applications, manage users, and monitor loan activity from one place.

Step 7: Integrate third-party services

Since lending app development foresees different financial procedures, integration of third-party tools or software is essential. Think of payment gateway integrations, bank account connections, bank cards, e-wallets, and accounting systems.

At this point, your app developer must connect your mobile application to the necessary tools using a set of APIs. Examine everything that needs to be integrated since the chosen tools and software will impact your loan app's functionality and security.

For a lending app, third-party integrations often go beyond payments. Teams also connect identity verification providers, credit scoring services, fraud prevention tools, e-signature solutions, notification services, and analytics platforms. These services help automate core parts of the lending flow and reduce manual work on the lender’s side.

This step deserves extra attention because every integration affects not only the feature set, but also system stability, compliance, and data security. The more sensitive the data, the more carefully the integration should be planned and tested.

Step 8: Test and launch the product

Finally, when you're all set with the steps mentioned above, test your lending app to check its appearance, performance, and functionality. The team usually runs several types of testing, including functional testing, security checks, and performance testing, to make sure the system can handle real users and financial transactions.

If it proves to operate smoothly, launch it in the market. Many teams start with a limited release or pilot version to monitor how the product behaves under real conditions before scaling it further.

At this stage, pay attention to each review you receive to implement necessary modifications if needed. User feedback, analytics, and early usage patterns often highlight small issues or feature gaps that are easier to address right after launch.

We offer full-cycle financial software development services, from creating product development strategy to top-notch fintech services implementation.

Develop your fintech software with Uptech! 📲

Money Lending App Development: Legal Part

Once you think of developing a money lending app, the need to study the legal requirements arises. The tricky thing is that the legal regulations applied to money lending apps differ from region to region. And even from state to state. So if you don't want to accrue huge fines (and I'm sure you don't), check out the main regulations I listed below and follow them religiously.

EU data protection regulation: GDPR

If you start a money lending app in Europe, you must comply with GDPR laws.

GDPR regulates how companies collect, store, and process personal data. Lending apps usually handle sensitive financial information, so developers must implement strong data protection practices, clear user consent flows, and secure data storage.

If the app connects to bank accounts or payment infrastructure, developers also need to consider the PSD2 directive, which governs open banking and secure financial data access in the EU.

USA regulations: privacy and consumer lending laws

USA data protection regulations: CCPA (California Consumer Privacy Act), CFPB (Consumer Financial Protection Bureau), and Agencies with Fair Lending Authority (Regulatory or Enforcement).

Today, CCPA operates together with the California Privacy Rights Act (CPRA), which expanded consumer data rights and strengthened enforcement starting in 2023.

They are in place to protect the public from data sharing, selling, and other wrongful uses.

State-specific regulations, like the California Consumer Privacy Act, oblige creators to fulfill their requirements when developing software for California residents. Due to CCPA, users receive more personal data control, and financial transactions become safer.

In addition to privacy regulations, lending apps in the United States must comply with several consumer lending laws, including:

- Truth in Lending Act (TILA), which requires clear disclosure of loan terms and interest rates;

- Equal Credit Opportunity Act (ECOA), which prohibits discrimination in lending decisions;

- Fair Credit Reporting Act (FCRA), which regulates the use of credit data;

- Anti-Money Laundering (AML) and Know Your Customer (KYC) requirements.

Depending on the lending model, companies may also need state lending licenses.

Loan guidelines and options change frequently, so I recommend you hire a legal consultant to keep an eye on legal changes in the fintech segment you are working with.

How Much Does It Cost to Build a Money Lending App?

Loan lending app development cost can start from $40 000 to over $400 000. The range is wide because several factors affect the final budget, including the development team, the region where the team operates, and the complexity of the product.

If you want to get a rough estimate for your project, you can also use the Uptech app development cost calculator. It helps evaluate the approximate budget based on the platform, features, and development scope.

Below are the main factors that influence the cost.

Team

As I've mentioned above, you can hire freelancers as the cheapest option, which might cost you approximately $30,000-$60,000, depending on the scope. However, managing multiple freelancers can require additional coordination and project management on your side.

Working with an agency sets the price at around $100,000 and may reach $250,000+ for a full product with design, development, and testing included.

Hiring in-house is often the most expensive option because it includes salaries, recruitment, onboarding, and long-term employment costs.

Outsourcing to a software development company is often a balanced option. It provides access to an established team of developers, designers, and QA engineers while keeping development costs lower than building a full internal team.

For a more accurate app development cost estimate, feel free to contact us.

Region

Development costs also depend heavily on location. Teams in North America and Western Europe usually charge the highest rates, while Eastern Europe, Latin America, and South Asia offer lower development costs.

Typical hourly rates look roughly like this:

- North America: $100-$200/hour

- Western Europe: $80-$150/hour

- Eastern Europe: $40-$70/hour

- South Asia: $25-$50/hour

Because of the strong engineering talent and moderate rates, many fintech companies choose Eastern Europe for outsourcing financial software development.

App complexity

The final price also depends on the number of features and the technical complexity of the platform.

A basic lending MVP with core functionality (registration, loan application, approval flow, payment integration) may cost $40,000-$80,000.

A mid-level lending app with user verification, credit scoring integrations, dashboards, and analytics usually falls in the $80,000-$200,000 range.

A complex lending platform with advanced risk models, multiple loan products, admin panels, compliance tools, and integrations can exceed $200,000-$400,000+.

Design complexity, security requirements, and regulatory compliance can also increase the development budget. The same goes for integrating AI capabilities, e.g., fraud detection systems.

Money Lending App Development Challenges and Solutions

Below, I describe the main challenges of developing a money-lending app. Take a look:

The complexity of the industry

Just to have a notion of how complex mobile banking is, break down the challenges of traditional banking. Only security issues themselves demand a different and more delicate approach on a digital level, like varying legislation and often third-party integrations.

Digital lending platforms must also support identity verification, payment processing, credit checks, fraud detection, and secure storage of financial data. Each of these systems may come from a different provider and must work together without exposing security risks.

Solution

Plan the system architecture early and choose reliable third-party providers for payments, identity verification, and fraud prevention. A well-designed infrastructure helps avoid costly changes later in development.

Diversity of legal regulations

Make sure you meet the legal requirements of the region where your app is supposed to work. Security standards differ not just from country to country but also on a smaller scale, like states sometimes (the California Consumer Privacy Act, for example).

In addition to privacy laws, lending platforms often must comply with consumer lending rules, identity verification requirements, and anti-money laundering regulations.

Solution

Involve legal and compliance specialists early in the product planning stage. Many fintech teams also build compliance checks directly into the platform to ensure loan terms, disclosures, and user verification follow local regulations.

The need for financial expertise

Hire a financial advisor who can help you reach your financial goals, ranging from investment plans to developing marketing strategies that suit you best. This one doesn't entail any risk, but finding a dedicated professional genuinely interested in developing your money lending app is not easy.

Beyond business strategy, lending products require expertise in credit risk models, loan terms, repayment structures, and financial compliance.

Solution

Collaborate with fintech specialists or product teams that already have experience with financial products. Their knowledge helps define lending rules, risk assessment methods, and approval workflows.

Finding a bank or financial partner

Partner with an investor or a bank institution to get your business off the ground. Be aware that in the case of banks, there will be certain regulations you must comply with, followed by a range of financial procedures, before you can access the funds. Meanwhile, funding your business through investors doesn't foresee various legal adjustments but does consider possible diminishment in ownership, influence, or control.

Many lending apps rely on partnerships with regulated financial institutions to issue loans, process payments, or hold funds.

Solution

Establish partnerships with banks, licensed lenders, or Banking-as-a-Service providers. These partners can supply financial infrastructure while your platform focuses on the digital product and user experience.

Now you've seen how to build a loan app step by step and what aspects you should bear in mind. Besides many technical issues, collaboration and partnerships are imminent in any lasting project. As a dedicated product development team, Uptech has helped to deliver more than 200+ products to the market over 10 years of experience.

Contact our team to get your project going!